Presales & Leverage — Reimagining Token Launch

No chapters available

#3: Presales & Leverage — Reimagining Token Launch

In Article #1, Floors: A Design for Floor-Backed Tokens, we introduced the concept of tokens with monotonically increasing floor prices and previewed the core mathematical invariant.

In Article #2, Anatomy of Floors — How Permanent Price Support Actually Works, we explored how Floors flow fees to reserves and how the core invariant ensures solvency.

TL;DR

Floors transforms token launches from zero-sum speculation into leveraged accumulation with liquidation-free credit. Everyone starts at the same floor price, leverage amplifies positions without protocol liquidations, and supply-based vesting aligns all participants with sustainable growth.

The Fundamental Shift: From Extraction to Accumulation

Most token launches are structured around tiered discounts — seed, private, public — which often create incentives for early holders to exit quickly. The result can be heavy day-one supply pressure.

Floors flips this model. Presales happen at a single, flat entry price (the initial floor, P_0). Whether you commit 10 million, you enter at the same price. That price becomes the permanent redemption floor in the primary market:

-

No participant can redeem below their entry.

-

Downside is capped at the floor.

-

Upside remains uncapped as fee flows strengthen reserves over time.

In other words, the presale price is not just an allocation—it is the lowest possible price the token will ever have on the primary market.

The Credit Facility: Leverage Without Liquidations

Traditional leverage means constant anxiety: monitor your health factor, add collateral during downturns, pray you don't get liquidated in a flash crash. One bad wick and your position evaporates.

The Floors credit facility breaks from every DeFi lending protocol before it. Borrowing capacity is issued against floor value, not spot price. There are no protocol-triggered liquidations. Loans are open-term with a one-time origination fee—no periodic interest accrues.

How It Works

With loan-to-value ratio g, a holder locking S tokens at floor P_f can draw up to g · P_f · S in reserves (subject to the coverage check from Article #2). When the floor rises, borrowing capacity increases proportionally without adding collateral.

The math is elegantly simple. Lock 1000 tokens with a 900 in reserve assets. Use those reserves however you like—buy more tokens, deploy to other protocols, or hold stable assets. Your debt remains fixed at $900, and your collateral cannot be liquidated by the protocol because the floor price only rises on the primary market.

When the floor rises to 990 (at 90% LTV) without adding collateral. The same locked tokens now support more credit. This reflexive mechanism rewards patient participants—the longer you wait, the more the protocol works in your favor.

Locking vs. Staking: Critical Distinction

Locking (to borrow) is not staking. When you lock:

-

Your tokens remain in the Tier-0 supply S_0 (ensuring full backing is maintained), but are reclassified from S_free (redeemable) to S_locked

-

You can borrow up to g · P_f per token (consuming protocol headroom H)

-

You pay a one-time origination fee; you do not earn staking distributions while locked

-

Position stays encumbered until repayment

Staking (to earn fees) keeps tokens inside S_free (redeemable) and earns time-weighted fee distributions in reserve assets. You can sell anytime on the curve (weight resets on exit). We will deepen staking in the next article, #4.

Coverage Check Implementation

Recalling the coverage check from Article #2, with S_0,post denoting Tier-0 supply after applying any new locks in the draw bundle, a new draw ΔD is permitted only if:

Here, buffer is a fixed or function-of-size safety margin (e.g., bps of notional) set by governance. If the inequality fails, new borrows pause until floor elevation through fees/yield/LRE raises A_f or redemptions reduce S_0.

Looping: Recursive Leverage at the Floor

The true innovation emerges when you combine presales with the credit facility through looping strategies. Instead of committing $1000 to buy 1000 tokens, you can amplify your position through recursive borrowing and buying—all at the floor price.

The Mathematics of Looping

Let's formalize the leverage calculation:

- g = LTV ratio (e.g., 0.90)

- φ = effective per-loop fee rate (origination + trading fees, net of non-reinvestable splits)

- η = g(1 − φ) = reinvestment fraction per loop

Net leverage follows a geometric series:

Leverage sensitivity to parameters:

| LTV g | Fee φ | η = g(1 − φ) | Net leverage L_net = 1/(1 − η) |

|---|---|---|---|

| 0.90 | 3% | 0.873 | 7.87× |

| 0.90 | 4% | 0.864 | 7.35× |

| 0.85 | 3% | 0.825 | 5.71× |

This table demonstrates how ~7-8x net leverage is achievable across reasonable parameter ranges.

Presale Transaction Flow

The entire loop executes atomically in a single transaction or bounded batch:

-

User commits reserve → mints at P_0

-

Contract locks minted tokens

-

Borrow at LTV g against floor value (not spot)

-

Recycle borrow proceeds into more mints at P_0

-

Repeat steps 2-4 up to the loop cap; apply per-loop fee schedule

-

Non-leveraged mints unlock at launch; leveraged mints vest per supply milestones

This atomic bundling, combined with the multi-day presale window, largely neutralizes front-running and MEV extraction during the presale phase.

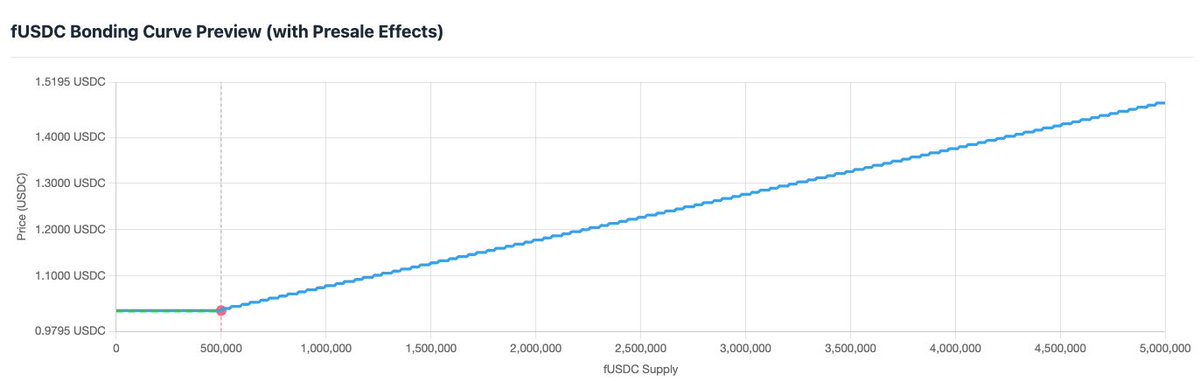

How Floors Presales Work

Consider a new token launching at a 1.00. These tokens remain locked until the presale ends.

The multi-day presale window serves a critical function: it eliminates presale-phase sandwich/front-run MEV by removing timing edges. Everyone has time to analyze, decide, and participate at their chosen leverage level without racing against bots or insiders during initial distribution. During presale, orders are commit-and-lock; there is no price-time priority to front run, so presale-phase sandwich and latency-arb MEV are structurally eliminated.

Once the period closes, the bonding curve activates with the floor permanently set at 1.01, 1000 on the primary curve—but redemptions on the primary market cannot settle below the floor price.

Canonical Example: Alex's Leveraged Launch Journey

Let's walk through a concrete example to illustrate how the mechanics work in practice.

Parameters:

-

Starting floor (held constant through presale): P_f = 0.01)

-

Initial reserves: L_f = $50,000; Initial Tier-0 supply: S_0 = 50,000

-

LTV: g = 95%; Origination fee: φ = 3% (on loan cash disbursed)

-

Coverage check (with P_f fixed at $1.00 held constant): A_post ≥ 1.00 · S_post

-

Commission on base deposit: 5%, paid additionally (does not reduce minted tokens)

-

Buy fee on each purchase (loops only): 0.5%

Important presale rule: During the entire presale, the published floor stays fixed at P_f = $1.00. Coverage checks and locking encumbrances use this constant value. Only after the presale closes is the new floor computed and published. This allows presale participants to loop at the same P_f.

Starting State (Pre-Presale)

-

A_f = L_f − D = 50,000

-

S_0 = 50,000

-

P_f = A_f / S_0 = 1.00 → P_f = 1.00** through the presale)

Step 0 — Base Deposit & Mint

Alex deposits 1.00 floor. A 5% commission ($500) is paid additionally to the protocol.

Effects:

-

Minted: 10,000 tokens

-

Reserves: L_f → 10,000 + 60,500**

-

Tier-0 supply: S_0 → 50,000 + 10,000 = 60,000

-

A_f = 0; Spendable: $60,500

-

P_f used for all presale actions remains $1.00

Presale Loops at Fixed P_f = $1.00

Each loop (single transaction) performs lock → borrow → mint using the borrowed cash.

-

Lock size: x tokens (remain in S_0 but move to S_locked)

-

Borrowed cash = 0.95x (valued at the fixed floor)

-

Origination fee = 3% of borrowed cash (retained by protocol)

-

Net cash spent on mint = borrowed cash − origination fee

-

Buy fee = 0.5% of the purchase; paid out of the spend; minted tokens = (net cash) / 1.005

-

Coverage Impact: Borrowing increases D and minting increases S_0. Unlike the simplified "denominator" models, Headroom () must remain non-negative. Looping is therefore constrained by the total available Headroom in the system.

During the presale, the protocol must be seeded with initial buffer or allocate non-refundable fees directly to reserves to create the Headroom () necessary to support leveraged positions.

Looping Mechanics (Conceptual)

- Start: User holds 10,000 tokens. Protocol has sufficient Buffer.

- Lock: User locks 10,000 tokens.

- Borrow: User draws reserve assets (Consumes Headroom).

- Mint: User mints new tokens (Adds to Reserves and Supply).

- Result: User multiplies exposure. Protocol maintains solvency via Headroom check.

Note: Since strictly includes locked tokens, deep looping (e.g. 7x) requires significant system Headroom (H), typically generated by seed capital or unclaimable fee revenue allocated to reserves. The "infinite loop" is structurally braked by the Coverage Check.

End of Presale — Recompute & Publish the New Floor

When presale closes, the protocol recomputes the final floor based on total spendable assets and total Tier-0 supply.

With participants looping (constrained by Headroom limits), the final floor price settles at a value fully backed by spendable reserves.

Unlocked tokens: If you stop after loop N, the last minted tranche (from loop N) is unlocked and free to trade (); all prior minted tranches are locked as collateral ().

Dynamic Fee Mechanisms

The protocol implements sophisticated fee mechanisms that scale with market conditions, ensuring value capture during high-activity periods while remaining competitive during normal operations.

External rate anchoring pulls reserve asset borrowing rates from multiple venues through oracle feeds. When USDC rates rise on Aave, Compound, and other majors, the protocol's origination fees adjust accordingly. This ensures competitive pricing while capturing appropriate value for credit without protocol liquidations.

Premium-responsive scaling increases fees based on M = P_spot/P_f. Base fees might sit at 0.5-1.0%, adding 0-400 basis points when M is high. This mechanism captures value during speculative frenzies while keeping costs low during accumulation phases.

Failure mode handling ensures robustness: Fees are bounded by governance-set min/max rails (e.g., 0.5-5.0% per loop). If oracles fail or become stale, the system reverts to base fees and may restrict new borrowing until data integrity returns.

Supply-Based Vesting: Protecting the Commons

Leverage without limits would destabilize any system. Floors implements supply-based vesting to ensure sustainable growth while preserving the benefits of amplified positions.

The Supply-Based Vesting Function

Notation:

-

S_0 = total supply at TGE

-

S(t) = total supply now (all tranches)

-

S_0 = total Tier-0 supply now (all tranches)

Define vesting tied to supply growth with cliff protection:

-

Choose cliff multiplier α (e.g., 1.5×) for minimum growth before any unlocks

-

Choose target multiplier λ (e.g., 3×) for full vesting completion

-

S_cliff = α · S_0 and S_1 = λ · S_0

Concrete Example

Imagine a token launches with:

S_0 = 1 million tokens after the presale ends. The protocol sets α = 1.5 (cliff) and λ = 3 (full vesting), creating these dynamics:

-

At launch to 1.49M supply: Claimable = 0%. All leveraged tokens remain completely locked

-

At 1.5M supply (cliff reached): Claimable = 0%. Vesting threshold achieved but no unlock yet

-

At 2M supply: Claimable = 33%. First meaningful unlock after substantial growth

-

At 2.25M supply: Claimable = 50%. Half unlocked

-

At 3M supply or beyond: Claimable = 100%. Your entire leveraged position is freely tradeable

KPI-Based Vesting: Floor Price as the North Star

Supply expansion can sometimes be gamed through wash trading or inorganic issuance. Floor price growth presents a more robust KPI because it directly reflects real economic value flowing into the protocol through fees, yield, and genuine trading activity. The floor only rises when actual value accumulates—it cannot be manipulated through circular trades or artificial volume.

The protocol can implement floor-price-gated vesting that creates even stronger alignment:

Where:

-

P_cliff = β · P_0 (e.g., β = 1.2 means 20% floor growth before cliff ends)

-

P_target = γ · P_0 (e.g., γ = 2.0 means 100% floor growth for full vesting)

Hybrid approach: Combine both metrics for maximum robustness. Tokens unlock based on whichever metric is more conservative:

This dual-gating ensures that leveraged participants only unlock when the protocol achieves both genuine growth (supply expansion) and real value accrual (floor elevation). Non-leveraged presale tokens unlock immediately when the presale ends.

Network Effects and Aligned Incentives

The advantage of Floors presales lies not just in individual mechanisms but in how they create self-reinforcing growth dynamics. Supply-based vesting transforms every leveraged participant into an active promoter—the faster the protocol grows and supply expands, the faster their tokens unlock. Floor-based vesting adds another layer: only real value accrual through fees and yield can unlock positions, ensuring participants focus on sustainable growth rather than empty metrics.

Higher leverage participation generates more fees that raise the floor, which attracts more participants seeking that guaranteed minimum, which drives more activity that unlocks vesting tokens faster.

Even the credit facility contributes to network effects—as the floor rises, existing loans become more capital efficient, demonstrating the model's superiority and attracting more sophisticated capital. Every participant, from day-one leveragers to patient holders to active traders, benefits from the success of others, creating a positive-sum game where individual incentives perfectly align with collective growth.

Real-World Applications

The combination of flat presales and liquidation-free leverage enables entirely new token distribution models:

DeFi protocols can launch with presale participants immediately able to borrow against their tokens to provide liquidity elsewhere. The floor design makes these tokens superior collateral compared to traditional volatile assets.

DAOs can launch with governance token holders able to leverage their positions for treasury operations while maintaining voting power through locked collateral.

Gaming tokens can provide players with immediate utility—use tokens as collateral to borrow operating capital while maintaining exposure to game success through floor appreciation.

RWA tokens gain immediate utility as borrowing collateral, with the credit facility providing bridge liquidity while real-world assets settle. The floor price reflects minimum asset value while markets discover appropriate premiums.

Initially, we will focus on network or governance tokens as collaterals for floor-backed token markets.

Why This Feels Different

Traditional token markets often feel zero-sum: early sellers rely on later buyers to exit, fueling adversarial boom-bust cycles.

Floors is designed for positive-sum cooperation. Every participant's activity helps raise the published floor—the programmatic redemption minimum used by the primary market.

-

Early participants benefit from appreciation and fee accrual that help ratchet the floor up over time.

-

Later participants enter at a higher floor level (i.e., a stronger downside bound), not looser security.

-

Stakers earn a configured share of protocol fees.

-

Borrowers pay origination fees that flow to reserves and lift the floor.

-

Arbitrageurs contribute via trading fees that also support floor elevation.

The rising floor changes the emotional arc from anxiety to anticipation. Instead of staring at charts with dread, holders watch fee accrual add another brick to the floor. With a known and improving downside bound, the cognitive burden of constant decision-making diminishes.

Key Considerations and Risks

Floors amplifies good tokens, not bad ones. The protocol transforms trading activity into permanent backing, but needs actual activity to work. A token with genuine utility and active trading might see its floor rise steadily from fees. A token nobody uses will see minimal floor growth—just passive yield trickling in. Think of Floors as infrastructure that makes good tokens better, not magic that fixes broken ones.

The floor price is your safety net on the primary market, not necessarily your market price. The protocol ensures you can always redeem at the floor on the primary market, but most trading happens above it on the bonding curve. Secondary markets may temporarily trade below the floor but are arbitraged toward convergence.

Like all DeFi, this is experimental technology. Smart contracts can have bugs. Yield strategies carry risks. Governance decisions matter. The regulatory landscape evolves. But the core mechanism is simple and verifiable onchain—you can always check the math yourself.

The Path Forward

Floors presales and leverage represent more than incremental improvements—they are fundamental reimagining of how tokens launch and how leverage works in DeFi. By starting entries at the contract-enforced floor, designing without protocol-triggered liquidations, and aligning all participants through fees that raise everyone's minimum value, the protocol creates dynamics where cooperation beats competition.

This is experimental technology with real risks. Smart contracts can have bugs. Leverage amplifies both gains and losses relative to fees paid. Market dynamics might differ from models. But the core innovation—everyone starts equal, nobody gets liquidated by the protocol, all activity raises the floor—offers a compelling alternative to extractive launch models that have dominated crypto since the beginning.

Next: Article #4: The Stakers—Patient Capital and Its Rewards explores how staking in Floors creates a new asset class that captures fee flows, enables credit access, and compounds value through time—all while maintaining liquidity through the bonding curve.

The revolution is not just rising floors. It is rising together.

Disclaimer

Floors Finance is experimental DeFi. Not investment advice. Participation involves significant risk, including possible total loss.

Full disclaimer: https://www.floors.finance/risk-disclosure

Published: October 15, 2025

Author: Floors Finance Team

Twitter: @FloorsFinance